How the 2026 rules work, why the thresholds keep pulling in more retirees, and the levers that bring the bill down

May 23, 2026

Most people spend their working lives watching Social Security taxes come out of every paycheck and assume that when the benefits finally start flowing the other direction, they'll arrive tax-free. For a lot of retirees, that turns out to be wrong. A meaningful share of the check can be pulled back into your taxable income, and the rules that decide how much are some of the least intuitive in the entire tax code.

I want to walk through how the tax actually works in 2026, why it quietly reaches more households every year, and --- most importantly --- the specific levers we use to soften it. There's also a new wrinkle this year worth understanding clearly, because it has been widely misread. The 2025 tax law created a temporary deduction for people 65 and older, and a lot of the coverage around it suggested Social Security is now untaxed. It isn't. The machinery underneath is unchanged. What changed is a separate deduction sitting on top of it.

One thing up front: this piece is educational. It is the framework, not a recommendation for your specific return. The numbers in your situation are a conversation with us, your CPA, and your tax preparer. With that said, let's look at the mechanics.

How the Tax Actually Works

The tax doesn't run off your total income the way most people assume. It runs off a special figure the IRS calls "combined income" --- sometimes called provisional income --- and the formula is specific: your adjusted gross income, plus any tax-exempt interest, plus one-half of your annual Social Security benefit.1 That half-of-your-benefit piece is what trips people up. Even income that never shows on your 1040, like interest from municipal bonds, gets added back into this calculation.1

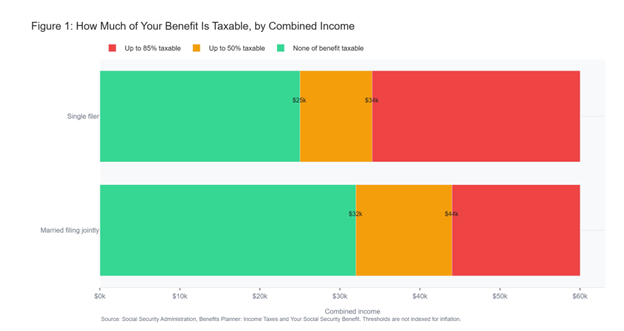

Once you have that combined-income figure, it runs through two thresholds. For a single filer, combined income below $25,000 means none of your benefit is taxed. Between $25,000 and $34,000, up to 50% of your benefit becomes taxable. Above $34,000, up to 85% of your benefit can be pulled into taxable income. For a married couple filing jointly, the same tiers apply at $32,000 and $44,000.1 Figure 1 lays out these bands.

A few things are worth emphasizing here. First, these percentages describe how much of your benefit is taxable --- not the tax rate. If 85% of a $40,000 benefit is taxable, that means $34,000 gets added to your ordinary income and is then taxed at whatever your marginal bracket happens to be. Second, 85% is the ceiling. No matter how high your income climbs, at least 15% of your Social Security benefit is always shielded from federal tax. The system was never designed to tax the whole check.

Figure 1: How much of your Social

Security benefit is taxable, by combined income and filing status. These

thresholds are fixed in statute and have never been adjusted for inflation.

Figure 1: How much of your Social

Security benefit is taxable, by combined income and filing status. These

thresholds are fixed in statute and have never been adjusted for inflation.

The Thresholds That Never Move

Here is the detail that matters most for long-term planning, and it's the one almost nobody knows: those threshold numbers --- $25,000, $32,000, $34,000, $44,000 --- have never been adjusted for inflation. They were written into law in the 1983 Social Security amendments and expanded in 1993, and they have sat frozen at those exact dollar figures ever since.1 Every other number in the tax code --- brackets, standard deductions, the estate exemption --- gets bumped up each year. These don't.

The consequence is a slow, deliberate kind of bracket creep. When the tax was first introduced, fewer than 10% of beneficiaries owed anything on their benefits. The Social Security Administration's own projections now estimate that an annual average of roughly 56% of beneficiary families will owe federal income tax on part of their benefits over the 2015-to-2050 window.2 Nothing about the law changed to produce that. Benefits rose with inflation --- the 2026 cost-of-living adjustment alone was 2.8%3 --- while the thresholds stayed put. Each year, a little more of the retired population crosses a line that was drawn in 1983 and never moved.

It's a bit like a doorway that's stayed the same height for forty years while everyone walking through it kept getting taller. Eventually most people have to duck. That's the design, whether intended or not, and it's why I treat managing combined income as a permanent part of retirement-income planning rather than a one-time calculation.

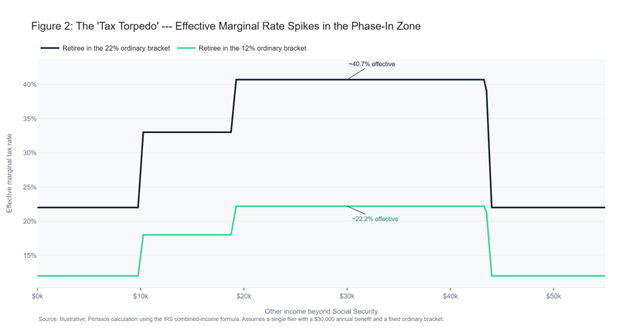

The Tax Torpedo

The frozen thresholds create a second, sneakier problem that planners call the "tax torpedo." Because each additional dollar of other income can drag more of your Social Security benefit into taxation, your effective marginal tax rate inside the phase-in range can be far higher than your stated bracket.

Let's look at the math. Suppose you're a single filer collecting a $30,000 benefit, and you take an extra $1,000 from your IRA. That $1,000 raises your combined income, which in turn pulls another $850 of your benefit into taxable income --- so you've now added $1,850 of taxable income for $1,000 of actual withdrawal. If you're in the 12% bracket, your real marginal rate on that withdrawal isn't 12%. It's 12% times 1.85, or about 22.2%. In the 22% bracket, the same arithmetic produces an effective rate north of 40%. Figure 2 shows how the marginal rate spikes through this zone and then settles back down once 85% of the benefit is fully taxed.

This is the single most important reason to think about retirement-income timing in advance. A retiree who stumbles into the torpedo zone with a poorly-timed IRA withdrawal can pay a startling rate on what looked like an ordinary distribution --- and never realize it, because the bill shows up as a slightly larger number on a line they don't scrutinize.

Figure 2: The 'tax torpedo.' Inside the phase-in zone, each added dollar of income pulls more of the benefit into taxation, lifting the effective marginal rate well above the stated bracket. Illustrative single filer with a $30,000 benefit.

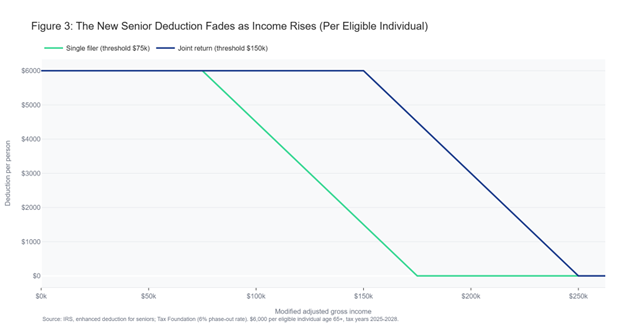

What 2026 Changed: The New Senior Deduction

This year there's a new piece on the board. The 2025 tax law created a temporary additional deduction of $6,000 for each taxpayer who is 65 or older, available for tax years 2025 through 2028. It's available whether you itemize or take the standard deduction, and it stacks on top of both the regular standard deduction --- $16,100 for a single filer and $32,200 for a married couple filing jointly in 2026 --- and the existing additional standard deduction for those 65 and up, which is $2,050 for a single filer and $1,650 per qualifying spouse this year.4 5

I want to be precise about what this deduction does and doesn't do, because the public coverage badly muddied it. It does not exempt Social Security from tax. The combined-income formula, the thresholds, and the 50%/85% tiers I described above are all completely unchanged. What the deduction does is lower your taxable income generally, which can indirectly reduce the tax you owe on the benefits that do get included. It's a deduction sitting on top of the existing system, not a repeal of it.

It also fades quickly for higher earners. The $6,000 is reduced by 6% of every dollar of modified adjusted gross income above $75,000 for a single filer or $150,000 for a couple, and it disappears entirely at $175,000 and $250,000 respectively.4 6 Figure 3 shows the per-person phase-down. For a married couple where both spouses are 65 or older, the deduction is $6,000 each --- $12,000 combined --- subject to that same income-based fade. And because it's written to expire after 2028, it's a four-year window, not a permanent feature. I treat it as a coupon with an expiration date taped to it: useful while it's here, but not something to build a permanent plan around.

Figure 3: The temporary senior deduction is worth $6,000 per eligible individual age 65 and older, then phases out at 6% of income above the filing-status threshold. Available for tax years 2025 through 2028.

Bringing the Bill Down

Now the part that matters: what you can actually do. Almost every lever comes back to the same idea --- managing your combined income, because that's the number the whole tax keys off of.

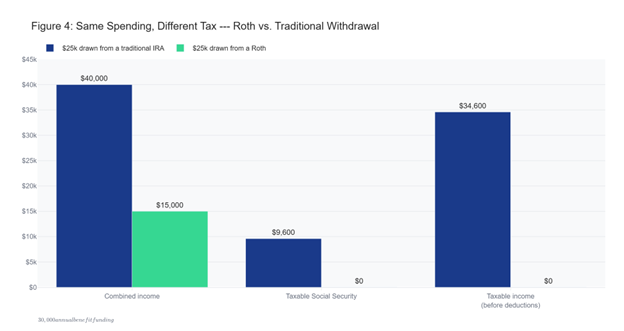

The most powerful tool is the Roth account, and the reason is mechanical. Qualified withdrawals from a Roth IRA don't appear in your adjusted gross income at all, which means they never enter the combined-income formula. A retiree who can fund part of a year's spending from a Roth rather than a traditional IRA keeps provisional income down and can keep more of the Social Security benefit out of taxable income entirely. Figure 4 illustrates this with a single filer drawing $25,000 of spending on top of a $30,000 benefit: pulling that $25,000 from a traditional IRA pushes combined income to $40,000 and makes $9,600 of the benefit taxable, while pulling the identical amount from a Roth leaves combined income low enough that none of the benefit is taxed. Same spending, very different tax outcome.

That points to the second lever, which is the multi-year Roth conversion strategy. The years between retirement and the start of required minimum distributions --- often your early-to-mid sixties through age 73 --- are frequently the lowest-income years of your life. Converting traditional IRA dollars to Roth in those gap years does two things at once: it fills up the lower brackets while they're empty, and it shrinks the future traditional balance that will eventually generate RMDs and inflate your combined income later. It's like buying down a future tax bill while it's on sale. The conversion is a multi-year decision, not a single-year one, and the right amount each year depends on where the bracket and threshold lines fall for you.

The third lever, for the charitably inclined who are 70-and-a-half or older, is the qualified charitable distribution. A gift sent directly from your IRA to a charity satisfies your required minimum distribution but never passes through your adjusted gross income --- so unlike a normal RMD, it doesn't push your combined income up toward the Social Security thresholds. For a retiree who gives anyway, routing the gift through the IRA rather than writing a check from a taxable account is often the more tax-efficient path.

A fourth point is really a caution: be careful assuming municipal bonds keep you under the radar. Tax-exempt interest is explicitly added back into the combined-income formula.1 Muni interest avoids ordinary income tax, but it does not avoid counting toward the taxation of your Social Security. It's a common surprise, and it's worth knowing before you build a retirement income portfolio around it.

Finally, there's the question of

when to claim. Delaying Social Security raises the eventual benefit, which can

mean more dollars exposed to the 85% inclusion later --- but it also shrinks

the years you're drawing from taxable accounts and can open a wider

Roth-conversion window beforehand. The claiming decision and the tax decision

are tangled together, which is exactly why I don't look at either one in

isolation. Figure 4: A single filer with a $30,000

benefit funds $25,000 of spending. Drawing from a Roth keeps combined income

low enough that none of the benefit is taxed; drawing from a traditional IRA

makes $9,600 of it taxable. Illustrative.

Figure 4: A single filer with a $30,000

benefit funds $25,000 of spending. Drawing from a Roth keeps combined income

low enough that none of the benefit is taxed; drawing from a traditional IRA

makes $9,600 of it taxable. Illustrative.

How We Approach This

None of these levers works as a standalone trick. The reason is that they interact --- a Roth conversion that looks smart in a vacuum can trip the tax torpedo or push you into a higher Medicare premium tier if it's sized wrong, and a claiming decision made purely to maximize the benefit can quietly raise the lifetime tax on that same benefit. We take a long-horizon, multi-year view precisely because these pieces only make sense together.

Our approach is tax-aware, not tax-driven. The goal isn't to minimize the tax on your Social Security in any single year --- it's to minimize the total tax across your retirement while keeping the plan flexible. Sometimes that means deliberately taxing more of your benefit in a low-income year to convert at a favorable rate. Sometimes it means leaving a Roth untouched because the conversion math doesn't clear. The right answer is specific to your accounts, your income sources, your charitable intentions, and your state. We work it out alongside your CPA and tax preparer, because a decision like this shouldn't live inside one office.

The taxation of Social Security is a quiet drag that most retirees never see coming, built on thresholds that were frozen in place over forty years ago and catch a little more of the population every year. The new senior deduction softens the edge for the next few years, but it doesn't change the underlying machinery, and it won't last forever. What does last is the discipline of managing combined income --- through Roth dollars, well-timed conversions, charitable distributions, and an honest look at when to claim. Those levers are available to almost everyone, and used together over a multi-year horizon, they can meaningfully lower the lifetime tax on benefits you already earned. Our team will continue watching the rules, including what happens to the senior deduction after 2028, and we'll adjust as the lines move.

All my best,

Brandon VanLandingham, CFA, CMT, CFP

Founder / CIO

Important Disclosures

This piece is educational. It is not legal, tax, or accounting advice and is not a recommendation to take or refrain from any specific action. Tax law is fact-specific and changes regularly. Please coordinate any decisions discussed here with your attorney, your CPA, and Perissos before acting.

Perissos Private Wealth Management is a Registered Investment Adviser ("RIA"). Registration as an investment adviser does not imply a certain level of skill or training, and the content of this communication has not been approved or verified by the United States Securities and Exchange Commission or by any state securities authority. Perissos Private Wealth Management renders individualized investment advice to persons in a particular state only after complying with the state's regulatory requirements, or pursuant to an applicable state exemption or exclusion. All investments carry risk, and no investment strategy can guarantee a profit or protect from loss of capital. Past performance is not indicative of future results.

The information contained in this newsletter is intended to provide general information about market themes. It is not intended to offer investment advice. Investment advice will only be given after a client engages our services by executing the appropriate investment services agreement. Information regarding investment products and services is given solely to provide education regarding our investment philosophy and our strategies. You should not rely on any information provided in making investment decisions.

Market data, articles and other content in this material are based on generally available information and are believed to be reliable. Perissos Private Wealth Management does not guarantee the accuracy of the information contained in this material.

Perissos Private Wealth Management will provide all prospective clients with a copy of our current Form ADV, Part 2A (Disclosure Brochure), Part 2B (Supplemental Brochures), and Part 3 (Client Relationship Summary) prior to commencing an advisory relationship. You can also view these documents at any time at adviserinfo.sec.gov or by contacting us requesting a copy.

Citations

1. Social Security Administration, "Income Taxes and Your Social Security Benefit," Benefits Planner. https://www.ssa.gov/benefits/retirement/planner/taxes.html 2. Social Security Administration, Office of Retirement and Disability Policy, "Income Taxes on Social Security Benefits" (research summary). https://www.ssa.gov/policy/docs/research-summaries/income-taxes-on-benefits.html 3. Social Security Administration, "Social Security Announces 2.8 Percent Benefit Increase for 2026," October 24, 2025. https://www.ssa.gov/news/en/press/releases/2025-10-24.html 4. Internal Revenue Service, "Check your eligibility for the new enhanced deduction for seniors." https://www.irs.gov/newsroom/check-your-eligibility-for-the-new-enhanced-deduction-for-seniors 5. Internal Revenue Service, "IRS releases tax inflation adjustments for tax year 2026" (Revenue Procedure 2025-32). https://www.irs.gov/newsroom/irs-releases-tax-inflation-adjustments-for-tax-year-2026-including-amendments-from-the-one-big-beautiful-bill 6. Tax Foundation, "The OBBBA Senior Deduction Is Poorly Targeted Tax Relief." https://taxfoundation.org/blog/obbba-senior-deduction-tax-relief/

Explore topics

Share this article

Last reviewed: May 23, 2026